In terms of turnover and number of employees, the German logistics market is the third largest economic sector – behind the automotive industry and retail. This is hardly surprising: efficient and high-performance logistics are essential for the economy. A look at the figures shows just how important the sector really is.

LOGISTICS: A DEFINITION

Logistics means much more than just getting goods or people from point A to point B. Rather, modern logistics is a complex field of activity in which the planning, control, coordination, implementation and monitoring of various information and goods flows must be taken into account.

Enormous efforts are therefore required to ensure that a product is available to the customer at the right time, in the right place and in the right condition. Increasingly differentiated and distributed value chains require top performance in many areas. In addition, the requirements of the various sectors of the economy differ significantly.

Just-in-time and just-in-sequence deliveries for automotive production, for example, can only be met with the help of meticulous organization and control of the delivery processes. This means many small steps and manual operations before a product’s journey is complete. The figures provided by the logistics sector must be viewed against this complex background.

“Logistics is a system that ensures an optimal supply of materials, information, parts and modules for production – and on the other hand, of course, the markets – both within the company and across companies with suppliers and customers.”

(Logistics definition of the German Logistics Association BVL)

SALES, COMPANIES & EMPLOYEES

Since 1995, the Supply Chain Services (SCS) working group at the Fraunhofer Institute for Integrated Circuits IIS has been providing a comprehensive insight into the German and European logistics market with its “TOP 100 of Logistics”. The study is therefore one of the most important sources for tracking industry developments – both in detail and in the overall picture.

The latter has improved significantly again after the major challenges at the beginning of the coronavirus pandemic: while the logistics industry was still able to report considerable growth of 5% in 2021, increasing the market volume to EUR 294 billion, the trend in 2022 was once again pointing sharply upwards:

- A cross-sector turnover of around 319 billion euros means growth of 8.5% compared to 2021.

- This gives the German logistics sector a share of around 25% of the European market, which was worth EUR 1.115 billion in 2020.

A not inconsiderable part of this performance is attributable to the freight forwarding industry. With an annual turnover of 135 billion euros, it accounted for just over 42% of the total volume. Compared to the previous year (117.5 billion euros in 2020), this is also a large increase in turnover.

According to the German Freight Forwarding and Logistics Association (DSLV), pure providers of logistics services account for an estimated half of the turnover generated. This includes the transportation and handling of goods.

Employment figures remain above 3 million

Employment figures in logistics have also continued to develop positively. Compared to 2020, more than 100,000 people were added to the workforce. The number of employees rose in the warehousing and goods handling sector in particular, with over 60,000 new employees in this sector alone.

The total number of people employed in 2021 was therefore 3.36 million, making the logistics sector one of the most important employers in Germany. The freight forwarding sector alone employs 600,000 people.

Companies in the logistics sector

The number of companies in the logistics sector varies. According to surveys by the Federal Office for Goods Transport (as at November 2020), the following picture emerges between commercial freight transport and own-account transport:

- Nationwide, 46,902 companies were active in commercial freight transport. This includes freight transport requiring a permit (34,372), freight forwarding, logistics, warehousing and cargo handling (1,620), CEP services (400) and other activities (10,510).

- A total of 45,929 companies were included in the business transport sector. The activities here are much more diverse and range from construction to commercial hunting.

In total, the Federal Office for Goods Transport lists almost 93,000 companies that are active in commercial road haulage or own-account transport.

The BVL, on the other hand, speaks of 70,000 companies in the logistics services sector. The DSLV also states 3,000 forwarding and logistics service providers.

FREIGHT TRANSPORT: ROAD REMAINS THE MOST IMPORTANT TRANSPORT ROUTE

In the “Mautverkehr KOMPAKT” annual report for 2022, the Federal Office of Logistics and Mobility states the following about road freight transport mileage

“A downward trend in daily mileage can be seen over the course of the year. While in the first half of the year the adjusted 7-day average is largely above the 24-month average, this reverses in the second half of the year.”

In addition, mileage fell by 0.7% compared to 2021. However, this was still 1.4% above the average for 2020 and 2021. German vehicles continue to account for the largest share of toll-paying mileage: at just over 50%, the share has fallen by 2 percentage points compared to 2019.

Nevertheless, domestic mileage is far ahead of that of other countries of origin. The mileage of Polish vehicles is still the highest at 22 percent, while the other European countries have shares of between 3.8 percent (Romania, Lithuania) and 1.4 percent (Slovakia).

FREIGHT TRANSPORT: ROAD REMAINS THE MOST IMPORTANT TRANSPORT ROUTE

In the “Mautverkehr KOMPAKT” annual report for 2022, the Federal Office of Logistics and Mobility states the following about road freight transport mileage

“A downward trend in daily mileage can be seen over the course of the year. While in the first half of the year the adjusted 7-day average is largely above the 24-month average, this reverses in the second half of the year.”

In addition, mileage fell by 0.7% compared to 2021. However, this was still 1.4% above the average for 2020 and 2021. German vehicles continue to account for the largest share of toll-paying mileage: at just over 50%, the share has fallen by 2 percentage points compared to 2019.

Nevertheless, domestic mileage is far ahead of that of other countries of origin. The mileage of Polish vehicles is still the highest at 22 percent, while the other European countries have shares of between 3.8 percent (Romania, Lithuania) and 1.4 percent (Slovakia).

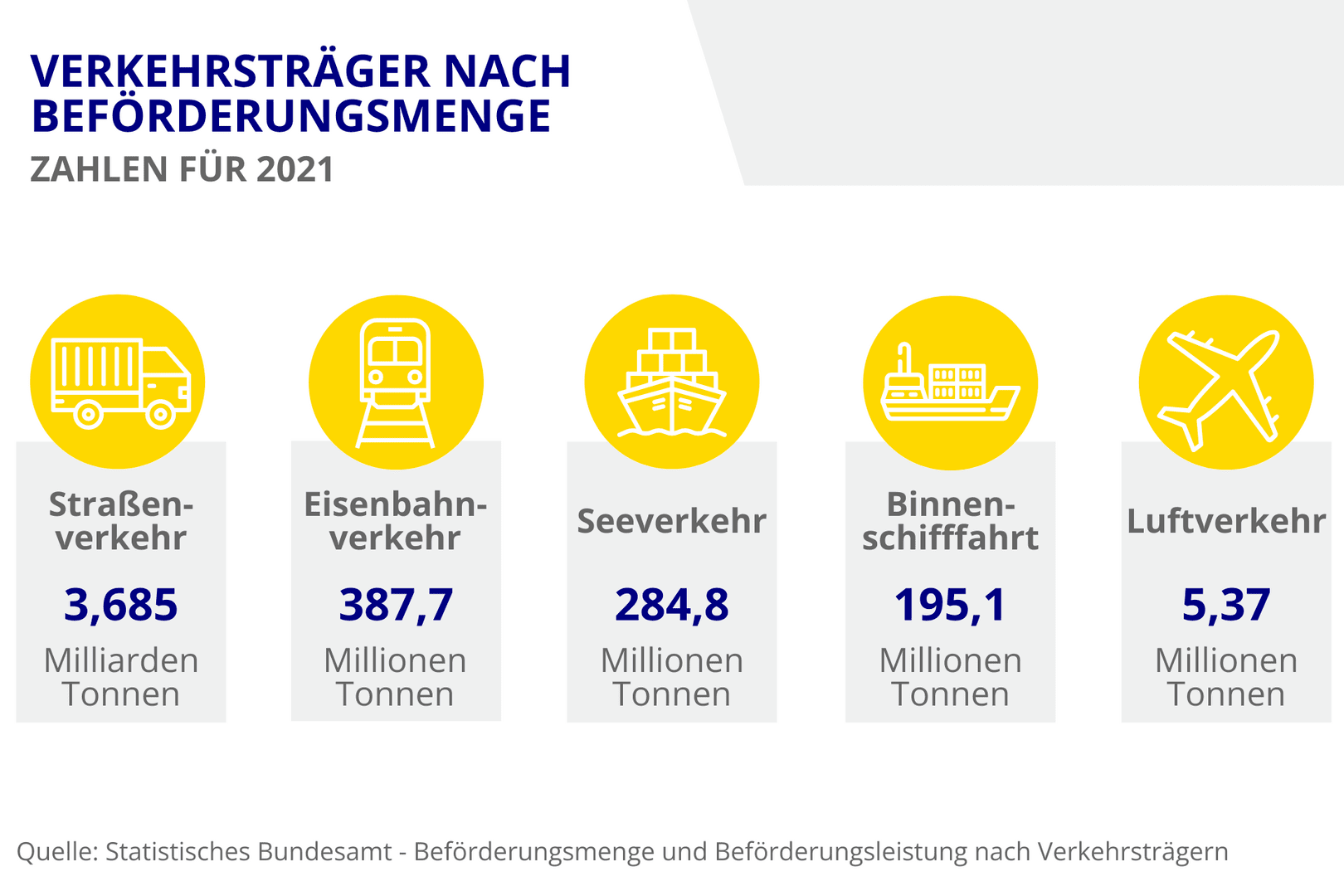

Road continues to lead the way in terms of transportation routes

When looking at the modes of transport or transport routes for freight transport, rail was one of the big winners in 2021: a transport volume of 387.7 million tons means growth of 13.5 percent compared to the previous year.

Despite significantly lower growth (2.5% compared to 2020), road freight transport remains the most important mode of transport. With a transport performance of 3.685 billion tons, road transport accounts for almost 79% of the transport volume.

According to the expectations of the Federal Ministry of Transport (BMDV), freight transport will continue to grow in the coming years. A long-term traffic forecast by the ministry assumes an increase of 46 percent by 2051, with trucks playing a decisive role in this scenario.

This is not least due to the fact that, according to the study, the focus of transported goods could shift. Instead of bulk and energy goods, the proportion of postal consignments, groupage and general cargo – i.e. those groups of goods that are primarily transported by road – is set to increase significantly.

SUBMARKETS OF THE LOGISTICS SECTOR

Although the transportation of goods is a central core area of logistics, it is by no means the only branch of the industry. In fact, the growing demands of the tasks involved have led to the “classic” range of transport, handling, storage and customs clearance services now being much more differentiated and diverse.

According to Fraunhofer SCS, transportation still accounts for 45% of the total volume of the logistics market. Warehousing and handling account for 33 percent, while inventories (15 percent) and administrative activities (7 percent) make up a much smaller share.

#

+

Contract logistics continues to gain in importance

Nevertheless, the logistics associations point to the growing importance of other business areas. In addition to specialized logistics submarkets, logistics services in particular are part of the repertoire of many companies.

Digitalization has opened up many opportunities to offer a broader portfolio of services, particularly in the area of contract logistics. At 80 billion euros, this form of service is one of the highest-turnover business areas in the German logistics sector.

“Value-added services are playing an increasingly important role in the logistics business. These are services that are tailored precisely to a specific customer. The type of services covers a broad spectrum, as the DSLV shows. Among other things, companies offer

- Logistics consulting,

- Picking and packing,

- Labeling,

- Tracking and tracing,

- Inventory management,

- Quality controls,

- Central warehouse function,

- Packaging,

- Order processing,

- Call-off control,

- Returns management,

- Control of air and sea freight,

- Assembly work,

- Invoicing and debt collection,

- Shelf service,

- E-fulfillment,

- Call Center and some others.

Logistics consulting (75%) and picking/packaging (67%) account for the largest share, ahead of labeling (54%) and tracking/tracing (49%). Contract logistics is an example of how far-reaching and extensive the topic of logistics is beyond the transportation of goods.

Specialization in demand: further submarkets and business areas

This can also be seen in the many other submarkets in which logistics companies provide their sometimes very specialized services. The reason for this is the often very specific requirements that companies from other sectors of the economy place on logistics.

Industry conditions, goods characteristics or forms of distribution have therefore led to a specialization of logistics companies. Accordingly, there is a wide spread of service focuses and areas in the various logistics submarkets:

| Service focus | Service area | |

| Trade logistics | 53 | 68 |

| Automotive logistics/automotive | 30 | 47 |

| Food and beverages | 27 | 43 |

| Mechanical engineering | 22 | 42 |

| Chemical logistics/hazardous goods | 25 | 41 |

| Spare parts logistics | 24 | 40 |

| Textile logistics | 18 | 28 |

| High-tech products | 16 | 32 |

| Temperature-controlled goods | 15 | 28 |

| Pharmaceutical logistics | 11 | 21 |

| (shares in percent) | ||

As the DSLV figures show, retail-related logistics is the most important submarket. Just over half of logistics companies focus on this sector, with a total of 68% offering services in this area. This puts retail logistics well ahead of the other submarkets.

Alongside the construction industry and the food sector, e-commerce recorded the highest growth rates. This is a continuation of the trend that was already evident before coronavirus.

The Fraunhofer SCS study “TOP 100 of Logistics” breaks down the market segments for the logistics industry even further and thus provides an insight into the respective market volumes:

- SMEs In-house logistics (44 billion euros)

- General cargo FTL (36 billion euros)

- Global air and sea freight logistics (33 billion euros)

- CEP services (27.4 billion euros)

- Cargo transportation with special equipment (20.1 billion euros)

- Bulk goods logistics (16.5 billion euros)

- Terminal, warehousing and other value-added services (EUR 15 billion)

- General groupage network transports (12 billion euros)

- Network transports for special general cargo (10 billion euros)

Overall, the Fraunhofer SCS sees the statistical findings as a positive sign for the German logistics industry. Despite the crises of recent years, it looks as if the sector remains stable. However, the challenges for global supply chains have also made it clear that logistics must adapt more strongly to the VUCA concept (Volatility, Uncertainty, Complexity, Ambiguity).

In this context, digitalization and artificial intelligence are mentioned as possible solutions to better prepare for increasing volatility, uncertainty, complexity and ambiguity in the future. As the backbone of industry and trade, the logistics sector will certainly retain its economic importance. However, the way in which it fulfills this role is likely to change in line with the growing demands on supply and value chains.

Image 1: Adobe Stock © photoschmidt

Image 2: Adobe Stock © Petinovs

Image 3: Adobe Stock © a_medvedkov

Image 4: Adobe Stock © thomaslerchphoto